What is a SWP Calculator?

A Systematic Withdrawal Plan (SWP) Calculator is a free online financial tool that helps you estimate how long your mutual fund corpus will last or what your remaining balance will be after regular withdrawals. It works by simulating monthly compounding on your invested amount and deducting a fixed withdrawal each month.

Unlike SIPs where you invest monthly, SWPs are about withdrawing a fixed sum from your investment while the remaining corpus continues to grow.

The Business Day SWP Calculator shows your total amount withdrawn, ending balance, and net profit or loss, giving you a clear view of your post-retirement or regular-income planning.

How can a SWP Calculator help you?

A SWP calculator helps investors plan consistent income and financial stability during retirement or other phases where steady cash flow is needed.

Here’s how it helps:

- 📊 Visual clarity: See how your corpus changes every year based on returns and withdrawals.

- 💡 Smart income planning: Choose the ideal withdrawal amount that lasts the entire investment period.

- ⏳ Avoid depletion: Know when your funds may run out if withdrawals exceed returns.

- 💰 Compare scenarios: Test different withdrawal amounts or durations instantly.

- 🧾 Tax-efficient planning: Use insights to select funds that minimize capital-gains impact.

It’s the perfect planning companion for retirees, freelancers, or anyone seeking steady periodic income from mutual funds.

How does an SWP Calculator work?

The calculator uses the concept of monthly compounding and fixed withdrawals.

🧮 Formula:

Where:

- P = Total investment amount

- W = Monthly withdrawal amount

- r = Monthly rate of return (annual rate ÷ 12 ÷ 100)

- n = Total number of months

This formula compounds your investment each month and subtracts the fixed withdrawal after growth.

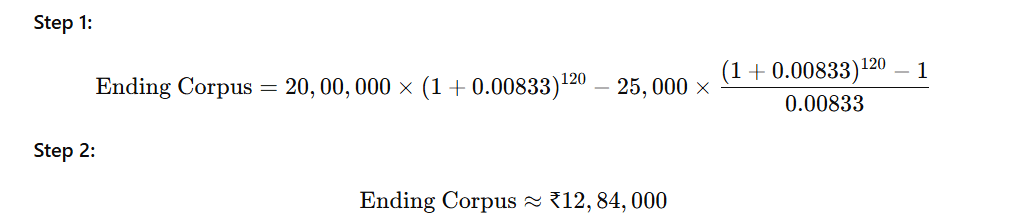

Example

| Parameter | Value |

|---|---|

| Total Investment (P) | ₹20,00,000 |

| Monthly Withdrawal (W) | ₹25,000 |

| Expected Return | 10% per annum (0.833% per month) |

| Duration | 10 years (120 months) |

| Calculation Type | Amount |

|---|---|

| Total Withdrawn | ₹30,00,000 |

| Ending Corpus | ₹12,84,000 |

| Net Growth (Interest) | ₹-7,16,000 (partial depletion over time) |

✅ This means after withdrawing ₹25,000 monthly for 10 years, you would have received ₹30 lakh in total and still have ₹12.84 lakh invested at the end — assuming a 10% annual return.

How to use the Business Day SWP Calculator?

Using the Business Day SWP Calculator is simple and interactive:

- Enter your total investment (₹) – the amount you’ve already invested.

- Add your monthly withdrawal (₹) – the amount you plan to receive every month.

- Enter expected return (% per annum) – the estimated growth rate of your mutual fund.

- Choose duration (years) – how long you want to continue withdrawals.

- Click “Calculate.”

The tool instantly displays:

- Total Withdrawn

- Ending Corpus

- Net Growth

- Graphs (line + donut) showing your corpus over time and withdrawal ratio.

The clean, red-white interface and Indian number formatting make it easy to understand results at a glance.

Advantages of using Business Day SWP Calculator

- ⚙️ Free & instant results: No sign-up or login required.

- 📈 Dynamic charts: See corpus reduction and withdrawal distribution visually.

- 💡 Goal-based analysis: Helps decide the ideal withdrawal amount for retirement or fixed income needs.

- 🧮 Accurate formula simulation: Based on monthly compounding for realistic projections.

- 📊 Data transparency: All calculations are client-side — no data stored on the server.

- 🧠 SEO-optimized insights: Built for mutual fund investors, advisors, and planners alike.

The Business Day SWP Calculator is your go-to tool to plan sustainable withdrawals, prevent premature corpus depletion, and make smarter post-retirement financial decisions.