What is EPF?

The Employees’ Provident Fund (EPF) is a government-backed retirement savings scheme in India managed by the Employees’ Provident Fund Organisation (EPFO).

Under the EPF & Miscellaneous Provisions Act, 1952, both the employee and employer contribute a fixed percentage of the employee’s basic salary and dearness allowance (DA) every month to build a retirement corpus.

Typically, the employee contributes 12% of their salary, and the employer matches this contribution. A portion of the employer’s share (8.33%) goes to the Employees’ Pension Scheme (EPS), while the remainder adds to the EPF balance. The accumulated funds earn annual interest declared by the government — usually between 8% and 8.5%, ensuring long-term wealth growth for salaried individuals.

What is an EPF Calculator?

An EPF Calculator is an online tool that helps employees estimate their retirement corpus, employer contributions, and interest earnings based on salary, contribution rates, and tenure.

It eliminates manual calculations by automatically applying the official EPF interest rate, compounding rules, and wage ceiling for EPS.

Using a calculator like the Business Day EPF Calculator, you can easily forecast your total accumulated EPF balance and plan your financial future more accurately.

How can an EPF Calculator Help You?

An EPF calculator provides a realistic projection of your savings and helps you:

- Understand how much wealth you’ll accumulate by retirement.

- Separate employee and employer contributions clearly.

- View interest earned on EPF in an easy-to-read chart.

- Adjust salary growth, tenure, or increment rate to see their impact.

- Make informed financial decisions for retirement, housing, or emergency planning.

By visualizing your EPF corpus year-by-year, the calculator empowers you to plan investments beyond mandatory savings.

Tax Treatment of Employee Provident Fund Contributions

EPF is one of the most tax-friendly retirement schemes under the EEE (Exempt-Exempt-Exempt) category:

- Employee contribution: Eligible for deduction under Section 80C (up to ₹1.5 lakh per financial year).

- Employer contribution: Not taxable up to 12% of basic salary.

- Interest earned: Tax-free as long as it does not exceed 9.5% per annum.

- Maturity amount: Fully exempt if the employee has completed five years of continuous service.

Thus, EPF not only helps you save for retirement but also provides excellent tax savings during your working life.

The Formula to Determine EPF Amount

The EPF contribution is calculated using a simple percentage formula:

Employee EPF=Basic Salary×12%

Employer EPF=Basic Salary×3.67%

Employer EPS=Basic Salary (max ₹15,000)×8.33%

Both the employee and employer EPF shares earn interest at the government-declared rate, compounded monthly. The EPS portion does not earn interest but builds your pensionable service.

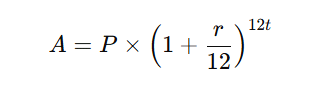

How Does an EPF Calculator Work?

An EPF calculator applies the monthly compounding formula to estimate your final corpus:

Where:

- A = Maturity amount after time t

- P = Monthly contribution (Employee + Employer EPF portions)

- r = Annual interest rate (%)

- t = Investment duration (in years)

Example

| Parameter | Value |

|---|---|

| Monthly Basic + DA | ₹30,000 |

| Employee EPF (12%) | ₹3,600 |

| Employer EPF (3.67%) | ₹1,101 |

| Employer EPS (8.33%) | ₹2,499 |

| Annual Interest Rate | 8.25% |

| Duration | 15 years |

Monthly EPF contribution (Employee + Employer EPF) = ₹4,701

≈ ₹18,54,000 (EPF Maturity Value)

| Category | Amount |

|---|---|

| Total Employee EPF | ₹6,48,000 |

| Total Employer EPF | ₹1,98,000 |

| Total EPS (Pension) | ₹4,50,000 |

| Interest Earned | ₹10,08,000 |

| EPF Corpus | ₹18,54,000 |

Thus, after 15 years, the employee accumulates nearly ₹18.5 lakh in EPF, excluding pension benefits.

How to Use Business Day EPF Calculator

Using the Business Day EPF Calculator is simple:

- Enter your basic + DA (monthly salary).

- Enter employee & employer contribution rates (default 12%).

- Input annual EPF interest rate (e.g., 8.25%).

- Add your investment duration (in years).

- Optionally include an annual increment % if your salary grows yearly.

- Click “Calculate.”

The tool instantly displays:

- Employee & employer EPF totals

- Interest earned

- Maturity value with visual charts

- Separate EPS (pension) contribution

It’s fast, accurate, and 100% free to use.

Advantages of Using Business Day EPF Calculator

- Instant results: Calculate your EPF corpus within seconds.

- Interactive visuals: View detailed charts for better clarity.

- Goal planning: Plan retirement or job-change scenarios.

- Accurate formulas: Reflects EPF & EPS Act guidelines.

- Understand interest impact: See compounding benefits over time.

- Accessible & free: No signup, no cost — just results.

- Secure: Runs entirely in your browser; no data stored.

The Business Day EPF Calculator makes complex retirement projections simple, letting you plan a stress-free and financially secure future.